Impacts to Private Student Loan Repayment Performance

Impacts to Private Student Loan Repayment Performance

More Updates to Direct Federal Student Loans Besides Repayment Restart

For an overview of the many upcoming changes to the direct federal student loan program, click on these links to NPR and Inside Higher Education. I am here to give my opinion on the potential impacts to private student loan repayment performance from monthly payment calculation changes. One year from now, the income driven repayment plan under Biden's Saving on a Valuable Education (SAVE) program will reduce payments to 5% from 10% of income. This aspect of SAVE is projected to be implemented in July 2024 after the direct federal student loan repayment restarts in September 2023.

As a refresher, borrowers of direct federal student loans have not had to make a monthly payment for over 3 years without interest accruing. We know that direct federal student loans go back into repayment on September 1, 2023, with a first monthly payment due date in October. This is a credit negative for private student loan portfolios due to the negative impact to disposable income from the federal student loan payment restart. Some lenders believe that the high credit quality underwriting of their loans will insulate portfolios, however, any material reduction to disposable income will strain household budgets to varying degrees. Financial impacts are shown in my recent blog.

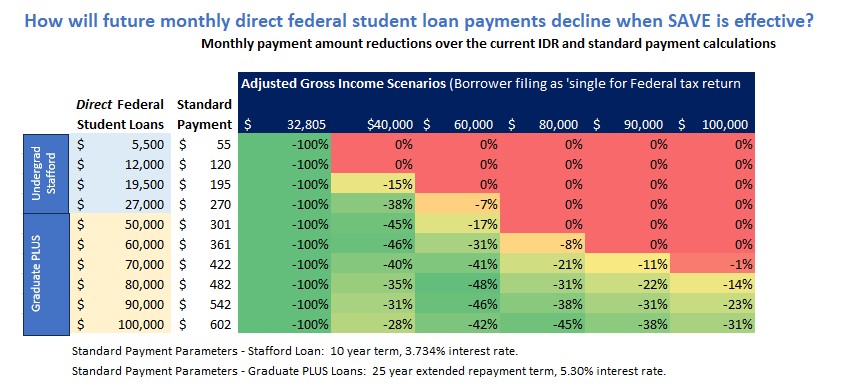

Higher Disposable Income of Direct Federal Student Loan Borrowers in July 2024?

The table above shows my analysis of potential monthly payment reductions to borrowers of direct federal student loans. Naturally a reduction in the monthly payment by a reduction in the income driven repayment plan from 10% of income to 5% of income will cut payments in half. However, higher incomes will reduce or disqualify some borrowers from a payment reduction. Another factor is the amount and type of direct federal student loan debt. The higher the debt, the more likely the borrower will have a payment amount reduction. The relationship of income and debt amounts will determine the amount of the payment reduction, if there is one at all.

Generally, borrowers with undergraduate degrees financed with direct federal Stafford loans will have minimal payment relief as incomes approach $60,000. For borrowers with graduate degrees financed with direct federal GradPLUS loans, they will have diminishing relief when incomes exceed $100,000. There are nuances (debts above $100,000), which means you should do your homework based on the incomes and direct federal student loan debt levels of borrowers in your loan portfolio.

Overall, the changes to the income driven repayment plan will be a credit positive to private student loan repayment performance starting in July 2024, but it will likely not be significant.

Will Borrower Disposable Income Improve to Benefit Private Student Loan Performance?

According to my analysis in the chart, borrowers with lower average incomes for their degree type will have more disposable income starting in July 2024 from the income driven repayment plan updated under the SAVE program. Graduate borrowers are likely to see the highest payment reductions given their high debt levels even when approaching average income levels.

The other factor is the participation rate for income driven repayment. According to the Inside Higher Education article that is referenced, the participation rate is only 30% now. The Education Department has a lot of work to do with an inadequate budget and operational constraints with their diminished third-party service providers.

Even with a sufficient budget and sufficient resources, program promotion would be a challenge due to the weak borrower and loan servicer relationship. Do borrowers even know who their direct federal servicer is at this point? Do servicers have updated email and address information to inform these borrowers of the income driven repayment program? Do borrowers have trust in their servicer? Enough said.

Private student loan lenders, loan servicers and student loan borrowers are in uncharted territory. Projections are futile. However, competent risk management depends on being prepared for negative outcomes.

Impacts to Private Student Loan Performance

As I already indicated in a prior blog, private student loan repayment performance will have higher delinquencies starting in Q4 2023 and into 2024. The payment relief starting in July 2024 will provide marginal benefits to improvements in disposable income for borrowers that are enrolled in the income driven repayment program. Low participation rates will reduce the upside, while borrowers that receive benefits are already below average in income and will continue to struggle to make payments on their private student loan.

Consulting by Einstein Higher Edu Solutions

Einstein Higher Edu Services provides deep domain expertise and advanced data analytic capabilities to optimize the management of risks to your traditional and new private student loan products. Risk expertise, machine learning, and loan program development are some areas where Einstein can provide lift to your organization. I look forward to having high-level decisions with private student loan lenders that are interested in this area or other areas.

Aaron Pisacane

Founder, Einstein Higher Edu Solutions

Affiliate sponsor of the Education Finance Council.

(917) 968-6483